Could the Housing Market be Approaching a Crisis Again

A Market review

for April 15th 2024

The content of this Newsletter is to provide you with Economic insights to assist you in making better decisions with your investments. Unlike many other financial periodicals we will not mention specific companies, unless it is relevant to an overall economic issue. We welcome your questions on economic concerns and will address in our newsletter. just email us at info@optfinancialstrategies.com #FinancialAdvisor,#investmentmanagement #wealthmanagement #financialplanning #retirementplanning #401kplans

Last week was one of the most volatile weeks of 2024, with all of the major indices posting declines for the 15th week of 2024. The largest decline was in the Russell 2000 with a -2.92% loss follow by the DOW -2.37% the S&P 500 index fell -1.6% and the NASDAQ -0.45%. All this downward movement came as higher-than-expected consumer price data and cautious guidance from JPMorgan Chase CEO Jamie Dimon added to market jitters. One other factor that may have contributed to the decline is tax week. Monday is April 15th and many tax payors may have liquidated their positions to pay their tax liabilities for 2023, however we can’t be sure just how much of this contributed to the steep decline. While all of the indices are down for the month and the start of Q2 they are still in positive territory YTD as you can see in the chart below.

Investors are eagerly waiting for signals from the Federal Reserve and the probability that the next move will be a rate cut in 2024 or a hike. Hopes for rate cuts have fueled much of the stock market's gains since Oct 27th of 2023 and in Q1 of this year. The March consumer price index on Wednesday came in much higher than expected, 3.48% YOY, prompting investors to curtail their prior optimism that rate cuts will start in June.

This week begins earnings season for Q1 2024, and Investors will be keeping a close eye on corporate results. On Friday JPMorgan reported better-than-expected Q1 earnings and revenue, but the bank raised its full-year expense outlook and maintained its 2024 net interest income outlook. Investors were disappointed by the lack of an increase in the net interest income guidance resulting in a decline of -6.5% JPMorgan’s shares, resulting in a weekly decline of -7.4%.

The Consumer Price Index rose 3.5% in March from the prior year, which was higher than expected and accelerated from 3.2% in February, as stubborn inflation continues to persist. The inflation rate measured by the core CPI, which excludes food and energy costs, did not improve for the first time since March of last year, holding at 3.8%. The report sent the 10-year Treasury yield above 4.5% for the first time since November, and chances of a rate cut at the Fed’s June meeting plummeted as the market grapples with high-for-longer interest rates. Producer prices rose less than expected in March from a year earlier, but the 2.1% increase was the highest in 11 months and an acceleration from February’s increase. The report offered further evidence that progress toward slowing inflation has stalled.

Following the inflation-driven selloff in government bonds earlier in the week, Treasury yields fell on Friday in a flight to safety set off by increasing geopolitical risks as Israel braced for an attack by Iran. Additional economic data released Friday showed that the University of Michigan’s Consumer Sentiment Index has remained steady this year despite missing expectations. Consumers noted little perceived economic change this year but increased their inflation expectations, reflecting frustration with the stalled inflation slowdown.

Sectors

Every sector in the S&P 500 fell this week, led by financials, which shed -3.6%, Healthcare and Materials sectors fell -3.1% Real Estate fell -3.06%. Technology, communications and Consumer Discretionary had the smallest declines, all under down by -1.0%.

The financial sector's decliners included shares of Globe Life (GL), which tumbled -46% as the life and supplemental health insurance company refuted what it described as "unsubstantiated" claims in a report by short-seller Fuzzy Panda Research alleging its executives disregarded insurance fraud.

Also in the financial sector, shares of Morgan Stanley (MS) fell -6.8% amid a Wall Street Journal report that the US Securities & Exchange Commission, the Office of the Comptroller of the Currency and other Treasury Department offices are investigating the bank over how it vets clients who are at risk of laundering money through its wealth-management division.

In the materials sector, shares of CF Industries Holdings (CF) shed -8.2% as BofA Securities downgraded its investment rating on the stock to neutral from buy. BofA Securities also lowered its price target on CF's stock to $88 each from $96.

Next week, companies expected to release quarterly earnings include Goldman Sachs Group (GS), Charles Schwab (SCHW), UnitedHealth Group (UNH), Johnson & Johnson (JNJ), Bank of America (BAC), Morgan Stanley, Abbott Laboratories (ABT), CSX Corp. (CSX), Netflix (NFLX), Procter & Gamble (PG) and American Express (AXP).

Is the Housing Market Approaching another Crisis ?

Homes are the cornerstone for most American’s balance sheet, in fact many Americans have found the value of their homes increased substantially since the 2008 GFC. Prior to 2008 many American purchased homes that were really outside their financial means, they had little equity in the home and often pulled out what little equity they may have had by refinancing their mortgage to pay for other things. In addition, bad mortgage brokers put these homebuyers in financial products, they did not understand, so homeowners got into financial trouble when the market corrected itself, this was one of the issues that contributed to the great financial crisis of 2008. However now homeowners are finding new issues that are impacting their homes.

Buying a home is more complicated than just affording the monthly mortgage payment and too often people will push the limits of what they can really afford, because they want a larger home, in a nicer area. In essence they gamble, becoming house rich and cash poor.

While most home buyers will take out a 30-year mortgage now when buying a home, a lesson learned during the 2008 crisis when most buyers were put in ARM’s (Adjustable-Rate Mortgage) which typically increase every year after the initial period (7 years) expires. One would think that from a budgetary perspective that a fixed 30-year expense would be easy to manage. Not quite.

Since the pandemic other expenses associated with home ownership have skyrocketed leaving many homeowners in a tight financial position. Non-mortgage costs including property taxes, maintenance, utilities and insurance make up more than half of homeowners’ overall costs, this is according to a 2022 analysis by Fannie Mae economists.

In addition, the cost of groceries which has increased +24.6% since the pandemic, dining out has increased more than +26% and was up +4.2% month over month in March alone. All adding more stress to the average family budget. These escalating costs on multiple fronts mean that many homeowners are being financially stretched.

Home ownership requires home insurance if you have a mortgage, these costs have increased 63% in just 2 years. Many of these increases have been the result of catastrophic events like fires and hurricanes and since insurance is based on diversifying risk by creating a pool when a major event depletes the pool, the funds need to be replenished by everyone even if the event is not in your area. If you are carrying a mortgage you are required to have insurance to cover the structure and very often the insurance premium is included in your mortgage since the bank will often pay that premium on the house alone (not personal property portion of the insurance)

We all realize that the cost of oil fluctuates and while current prices are up, many homeowners living in the northern states have been lucky for a few mild winters which has kept heating cost down but other utility expenses, such as electricity are up. In March alone utility costs increased more than +3.6% monthly. Another cost which impacts approximately a third of all homes are Association fees which are also up significantly for those living in communities that provide waste removal, and other maintenance costs.

These fees can range from a few hundred dollars a month to several hundred a month. These communities generally have strict by-laws and one of them could be losing your home if fees are too far in arrears. According to the community association institute delinquencies of more than 90 days are now above 5%. Traditionally, federal insurers Fannie Mae, Freddie Mac, and the Federal Housing Administration will not secure mortgages in communities with greater than 10% delinquency on association fees. This appears to be a rising problem.

But what is really alarming to many homeowners is the increase in property taxes. Property taxes are rising because of the effect of inflation on local government budgets, let alone those municipalities that are poorly governed. The average property tax for U.S. single-family homes was $4,062 in 2023, up 4.1% from 2022. However, many major metro areas like Chicago are contending with much bigger increases, which use its property taxes to meet it fiscal mismanagement requirements. Here the median residential tax bill increased more than +15.1% in 2023 mostly in the northwest suburbs of cook county. which already has double digit property tax rates. In Charlotte, N.C., the average property tax rose 31.5% from 2022 to 2023. In Indianapolis it was up nearly 19%. These are significant increases to families that thought their homes were affordable.

Keep in mind that there are 2 main components to property taxes, one is the tax rate a fixed amount and the other is the assessed value of the property. This is the subjective part of taxes that property owners can appeal to the tax board. So, while home values escalate so do their property taxes. But this value is not generally realized until you sell the home. Maintaining the expense while you are currently residing in the house is the challenge.

All these increasing expenses are pushing homeowners to dig deeper into their bank accounts and put more cost-of-living expenses on their credit cards. Now you know why credit card balances are at all-time highs.

There are just too many homeowners that are stretched financially and cannot meet these home-related expenses. According to tech company Clever Real Estate nearly one in five homeowners said they couldn’t afford a $500 emergency repair without going into credit-card debt, this from a February online survey of 1,000 homeowners, 42% said they’ve skipped home repairs or maintenance because of the cost. Lastly almost 10% of homeowners surveyed by Fannie Mae last year were not confident they could afford their home insurance premiums at their next renewal.

For many Americans inflation is just not a current short-term problem, unless we enter a deflationary period many Americans will struggle to maintain the cost of owning a home even with a low interest rate mortgage. The only solution will be to either make more money by getting a 2nd job or significantly changing their lifestyle and cutting back on discretionary spending. Source: https://www.wsj.com/economy/housing/housing-affordability-taxes-insurance-costs-rise-bca64df1?mod=hp_lead_pos7

A Technical Perspective

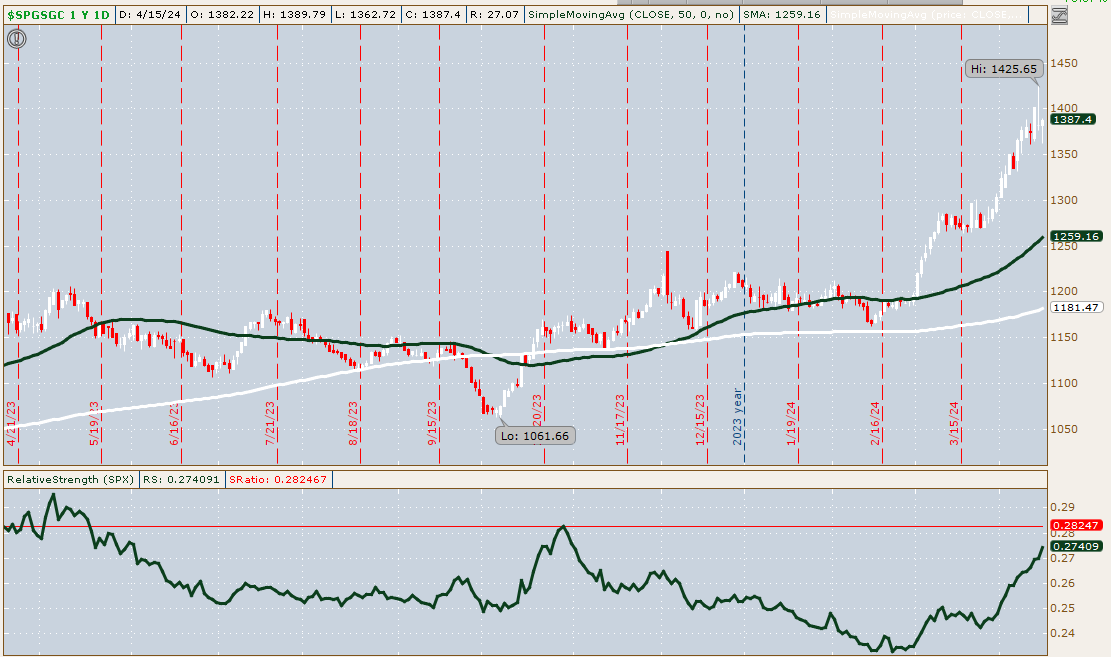

Even though we addressed Gold last week we wanted to take another look again. Gold reached another all-time high last week before reversing on Friday, despite the rising U.S. dollar and Treasury yields that often hinder commodity prices. Middle East tensions and central bank buying are likely the driving forces behind the continued momentum, as gold is considered a safe-haven asset.

The S&P GSCI Gold index ($SPGSGC) tracks the movements of gold futures, and from a technical perspective, price momentum remains positive. However, most oscillating indicators, such as the RSI, suggest extremely overbought conditions in the short term. An overbought reading isn’t necessarily a reversal signal—even if price falls and the RSI drops out of the overbought zone above 70, the intermediate-term bullish trend would likely remain in place. Fibonacci extensions are one way to identify potential technical support and resistance levels in this situation. Price has already exceeded 100% of the initial move from February 15 to March 11 by reaching above $1,390. If the uptrend continues, the index might push for the 161.8% extension near $1,470 as a potential target. Although gold’s overall trend is firmly bullish, any follow through from Friday’s bearish shooting star candlestick could spark heavy short-term selling.

The Week Ahead

After the March employment and CPI reports caused investors to drastically adjust their interest rate expectations, this week’s focus turns to first-quarter corporate earnings and a slew of second tier economic data. In the U.S., retail sales and the New York regional manufacturing survey start things off today. Following the recent inflation figures, any signs of economic strength or weakness could sway sentiment as to how the Fed might proceed. U.S. housing numbers will feature this week, with starts, building permits, and existing home sales on the docket. Additionally, homebuilder DR Horton will report earnings before the market opens on Thursday. Other companies announcing results this week include Netflix, Goldman Sachs, Bank of America, American Express, and Procter & Gamble. The rest of the U.S. calendar contains industrial production figures, the Philly Fed manufacturing index, and appearances from several FOMC members. Overseas, the main event will be China’s monthly data dump later tonight, including industrial production, retail sales, and GDP. Optimism for China’s economy has been building, but deflation and slumping exports remain problematic. In the UK, the employment report is due Tuesday, and a cooling labor market may provide some relief from wage pressures. British CPI and retail sales also arrive this week. Europe will be quiet, with Tuesday’s economic sentiment readings and Friday’s German producer prices the only items of interest. Last of all, the International Monetary Fund will hold its spring meetings in Washington after warning last week that global growth is threatened by high debt and geopolitical conflicts.

This article is provided by Gene Witt of FourStar Wealth Advisors, LLC (“FourStar” or the “Firm”) for general informational purposes only. This information is not considered to be an offer to buy or sell any securities or investments. Investing involves the risk of loss and investors should be prepared to bear potential losses. Investments should only be made after thorough review with your investment advisor, considering all factors including personal goals, needs and risk tolerance. FourStar is a SEC registered investment adviser that maintains a principal place of business in the State of Illinois. The Firm may only transact business in those states in which it is notice filed or qualifies for a corresponding exemption from such requirements. For information about FourStar’s registration status and business operations, please consult the Firm’s Form ADV disclosure documents, the most recent versions of which are available on the SEC’s Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov/

The Optimized Investor

CONTACT

320 W Ohio Street

Suite 328

Chicago IL 60654

312.263.1590 X 101

Gene@optfinancialstrategies.com

General Advertising Disclaimer This website is provided by Optimized Financial Strategies which is part of FourStar Wealth Advisors, LLC (“FourStar” or the “Firm”) for general informational purposes only. This information is not considered to be an offer to buy or sell any securities or investments. Investing involves the risk of loss and investors should be prepared to bear potential losses. Investments should only be made after thorough review with your investment advisor, considering all factors including personal goals, needs and risk tolerance. FourStar is a SEC registered investment adviser that maintains a principal place of business in the State of Illinois. The Firm may only transact business in those states in which it is notice filed or qualifies for a corresponding exemption from such requirements. For information about FourStar’s registration status and business operations, please consult the Firm’s Form ADV disclosure documents, the most recent versions of which are available on the SEC’s Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov/